The impressive numbers, laid out in the AEMO’s Integrated System Plan that was published on Monday night, put distributed solar, or DER, on track to supply more power to the national grid than coal within little more than 20 years.

They also demonstrate how silly it would be to have any sort of renewable energy target below 40 per cent by 2040, when distributed small-scale solar alone is expected to supply more than half of that number, and while there is an estimated 35GW of big solar also in the development pipeline – not to mention wind and hydro.

According to the ISP, in 2040 rooftop PV generation is projected to reach approximately 31TWh across the NEM in its Neutral (below), Slow change, and Fast change scenarios, and nearly 50TWh in the high DER scenario.

This represents between 13 and 22 per cent of forecast total underlying NEM electricity consumption, the report says, and has the potential to “deliver a major cost saving to consumers.”

How? In a number of ways, AEMO explains. For one, it would reduce the need for utility-scale renewable generation, thus cutting the costs associated with connecting these assets within the transmission system.

Efficiency gains associated with lowering overall system losses are also anticipated, the report says, as energy is generated at the point of consumption.

And perhaps most importantly, there is the impact that distributed solar and storage has on reducing local peak loads, providing network savings at both the transmission and distribution level, that can then be passed on to consumers.

These savings would be greatest, of course, under the ISP’s High DER scenario, which considers a future where distributed rooftop PV generation, battery storage, and other demand-based resources

at the consumer level are higher than in the Neutral case.

Indeed, AEMO says that the purpose of modelling the High DER scenario was to examine how increased distributed solar and storage could impact on – ie. reduce – investment needs for utility-scale generation and storage and transmission. (See chart above.)

By how much? The number AEMO came up with was significant: “High DER scenario shows the potential for even greater use of DER to lower the total costs to supply, with the net present value of wholesale resource costs reduced by nearly $4 billion, compared to the Neutral case.”

And the market operator seems fairly confident that the rooftop solar boom Australia has been enjoying is in no danger of slowing down.

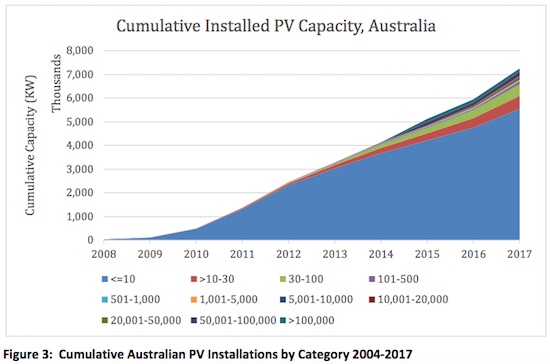

As the ISP report notes, installations have gone from a negligible amount in 2008, to an estimated 6GW-plus (across 1.6 million systems) by March 2018.

“This growth is assumed to continue as competitive pressures drive cost reductions and further innovation drives new commercial opportunities (either through new technologies or new consumer offerings),” the AEMO report says.

This assumption is backed up by the latest data from the Australian PV Institute, which puts the rooftop solar tally at 1.8 million systems, and notes that more than over 160,000 of that number were added in 2017, alone.

“Australia’s high electricity prices and inexpensive PV systems means payback can commonly be achieved in 3-5 years, a situation that looks set to continue in 2018,” the APVI report said.

“Momentum is building for further acceleration of commercial PV deployment, and corporate interest in solar PPAs is emerging.”

AEMO’s ISP assumptions about rooftop solar, and its potential to out-generate coal on Australia’s grid by 2040, also gel with a recent report from Bloomberg New Energy Finance, which said the biggest threat to the nation’s legacy coal-fired generators was not wind and solar farms, or even the settings of the country’s emissions policy, but the continued boom in rooftop solar.

BloombergNEF is more bullish than AEMO, however, forecasting a massive surge of “behind the meter” solar PV capacity, the big driver of which will not just be the household or “commercial” sectors, but the smaller business sector that is currently booming and will install nearly as much as homes.

It will also come from big industrial users, who are expected to account for nearly half of the 58GW that will be installed in Australia by 2050, and will be installing more than 2GW a year by the late 2020s, BloombergNEF said.

“There will be more capacity behind the meter than the total current capacity in the National Electricity Market (NEM),” lead analyst Kobad Bhavnagri told RenewEconomy after the presentation of the company’s New Energy Outlook in Sydney last week.

“It is a massive slab of capacity … and it will be the biggest single contributor to generation.”

Contact Sunstainable today to discuss going solar!